10s30s Steepener

Trade Idea

Current: 24.5bps

Entry: 35bps

Target: 57bps

Stop: 20bps

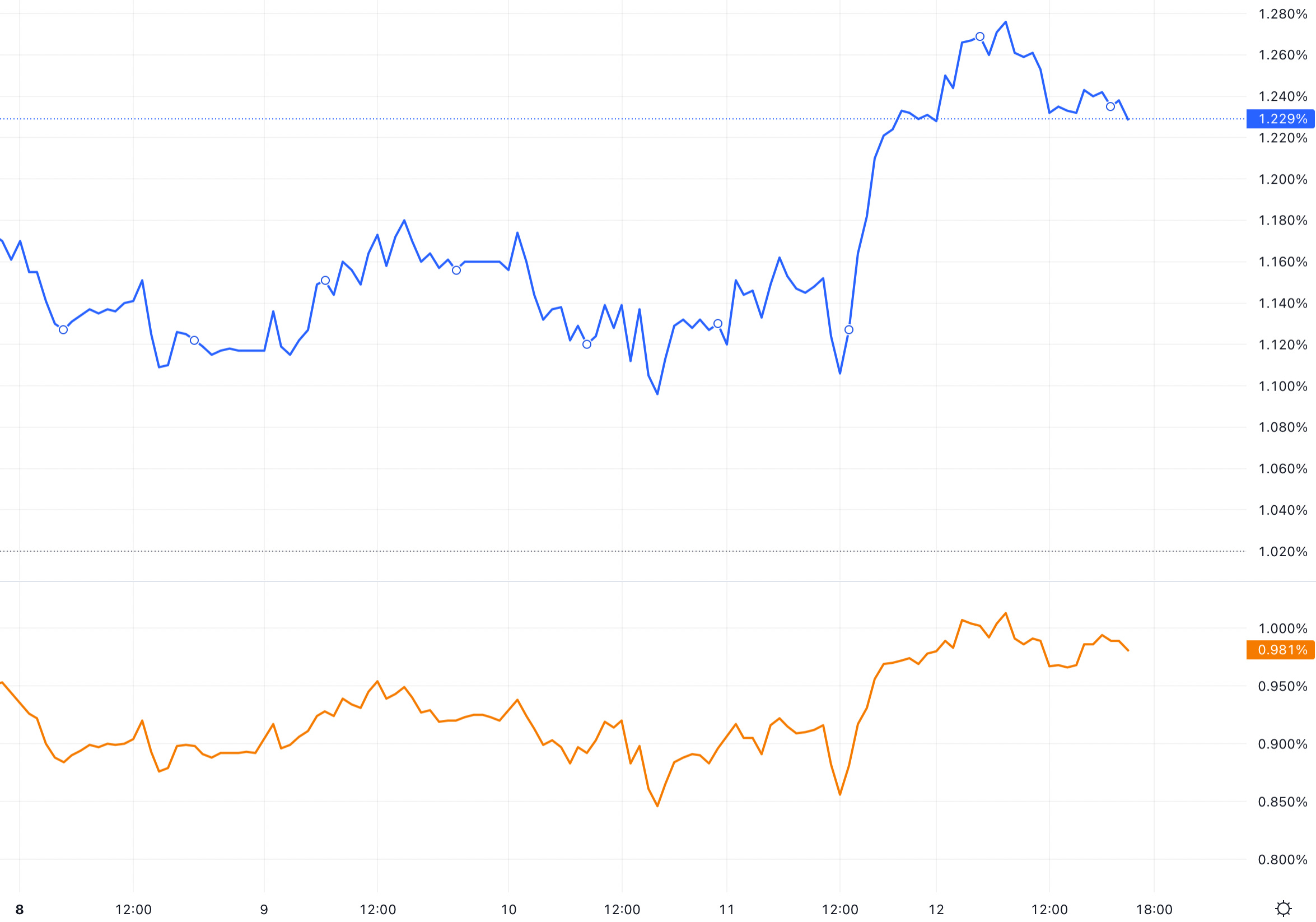

Here we see the German 30y curve at the top and the German 10y curve at the bottom:

Catalysts

Outperformance of EU GDP to US GDP

The latest GDP prints show that Eurozone GDP beat expectations by a landslide. Q/q growth in Q2 was up 0.7%, compared to a Bloomberg-consensus estimate of 0.2% growth. This is particularly interesting when noting the US GDP print for the same quarter. This surprised to the downside at -0.9% Q/q growth, underperforming estimates of +0.4% Q/q significantly.

The outperformance points to some alleviation of recessionary fears in the EU area. Heightened recessionary fears leads to Central Banks cutting rates at a nearer time-horizon, as expansionary monetary measures are needed in a time of slowing growth so that the economy does not fall into an unrecoverable position.

We may not expect the ECB to cut rates as soon as priced in, given the outperformance of some recessionary fears, and so we expect a flatter 2s10s curve, since short-term rates will stay elevated. This will support the steepening of the 10s30s.

Inflation persistence

A surprise to US CPI being unchanged at 8.5% for July 2022, compared to estimates of 8.7% for the same month was seen. While there is debates over whether this means current interest rate measures are starting to curb inflation and are enough to do so, the FED came out strongly saying inflation has not been controlled and will continue to be the prime focus.

This is a sentiment in-line with major G10 Central Banks, that the dual mandate of controlling inflation and growth is now transitioning to target inflation much more strongly. While the FED continues to hike rates, it seems likely the ECB will as well. The unchanged inflation print does not point to peaking inflation, as whether inflation has peaked is dependent on a number of factors.

Recent tensions with gas supply in Europe have heightened following comments from the Kremlin blaming the shortages in supply on Europe's sanctions on Russia. They stated it is these sanctions which impacted the maintenance of the turbines and was a self-inflicted crisis. There were concerns over further cuts; with Nord Stream 1 already at 20% capacity this would not be ideal as we approach winter. These concerns lead to further fears of heightening inflation, again supporting a 2s10s flattener and so a 10s30s steepener position.

Further, China's Zero-Covid policies have reduced exports and caused severe supply chain disruptions, another factor which has induced inflation in the Eurozone area.

TPI should support shorter maturity yields

The ECB recently released its long-awaited anti-fragmentation tool: the TPI. The Transmission Protection Instrument is a bond-buying mechanism to support Eurozone countries, as they struggle with the economic climate of rising rates and low issuance. The tool is focused on short-maturity bonds, of up to 10years.

The tool should decrease yields on these bonds, as higher demand through purchasing will increase the price of these bonds, and hence lower yields.

Since the ECB is focusing on shorter-maturity bonds, we expect the 10y yield to fall, since it is traditionally driven by technical factors.

A fall in the 10y yield will contribute to a 10s30s steepener.

Political Instability

Italy has been in headlines over the past month for the turmoil and uncertainty caused by its political crisis. You can read more about what caused the crisis in Draghi: Remain or Leave however what has followed is an anxious build-up to the elections on 5 September 2022.

It is increasingly likely the centre-right coalition will dominate the elections. This party has had traditionally federalist and eurosceptic views, and in the 2018 general election, there was even fears over a referendum for Italy to leave the EU.

Now manifestos have not been released for the parties, however there is concerns over the long-term outlook of Italy in particularly of this coalition coming into power, and how Italy will continue to interact with the EU.

We believe this will impose uncertainty and increases risks in the long-term, and so the 30y yields may rise, amidst the concerns over fiscal and monetary policy changes. Nevertheless, since this party is likely to be elected, we believe a 10s30s steepener position is the best outlook.

Risks

A potential risk we see to this trade:

Inflation stabilisation.

In a case when the Eurozone CPI readings start to steady and even decline M/m, there may be an earlier switch to smaller interest rate hikes and potential cuts. This would steepen the 2s10s curve, and lift 10y yields. However, we do not believe this is a severe risk at this stage, given the strong determination of major Central Banks to keep inflation under control and hike interest rates to do so. It is unlikely the ECB will cut rates in the next two quarters at least, especially supported by the Q2 growth readings.

Conclusion

We believe the ECB will continue to lift rates and so we stand-by the 10s30s steepener position.

In addition, we may implement a 2s10s30s fly position, to take advantage of the rising yields of the wings of the fly (2y and 30y yields) and the falling belly (10y yield). We want to enter at the belly to benefit from the rising 2y and 30y yields, both of which should push down the 10y yield. In addition, a surprise downside to 2y yield will be partially offset with the fly positioning and the rise in 30y yield counteracting that. Depending on the next CPI print we may prefer this position than an outright 10s30s steepener.