Corporate Bonds

Cheaper than ever

Interest hikes. It's everywhere. And it's great for loan holders; high interest payments is providing them higher cashflows. But how long can this be sustained, and when will the time inevitably come when loan issuers default on their payments. This may be sooner than we expect, and is causing banks to take massive hits.

When default risks increase, so-called credit risk, making the credit spread wider, yields on bonds rise and subsequently investors require discounts on bond prices. This is because of the inverse relation between yields and prices, and since the probability of default is higher, risk of holding the bond is higher. Higher returns on investments are required to justify holding a riskier asset, and due to the aforementioned price-yield relation, this collapses prices.

What the corporate bond world has seen recently, however, is an extreme movement in prices down, with bonds being offered at massive discounts to par. We categorise debt into two types:

Investment-grade bonds

High-yield bonds

Colloquially high-yield bonds are referred to as "junk bonds", and refer to bonds with lower credit ratings, as opposed to investment-grade bonds which command higher credit ratings, as provided by credit rating agencies such as Standard & Poor or Moodys.

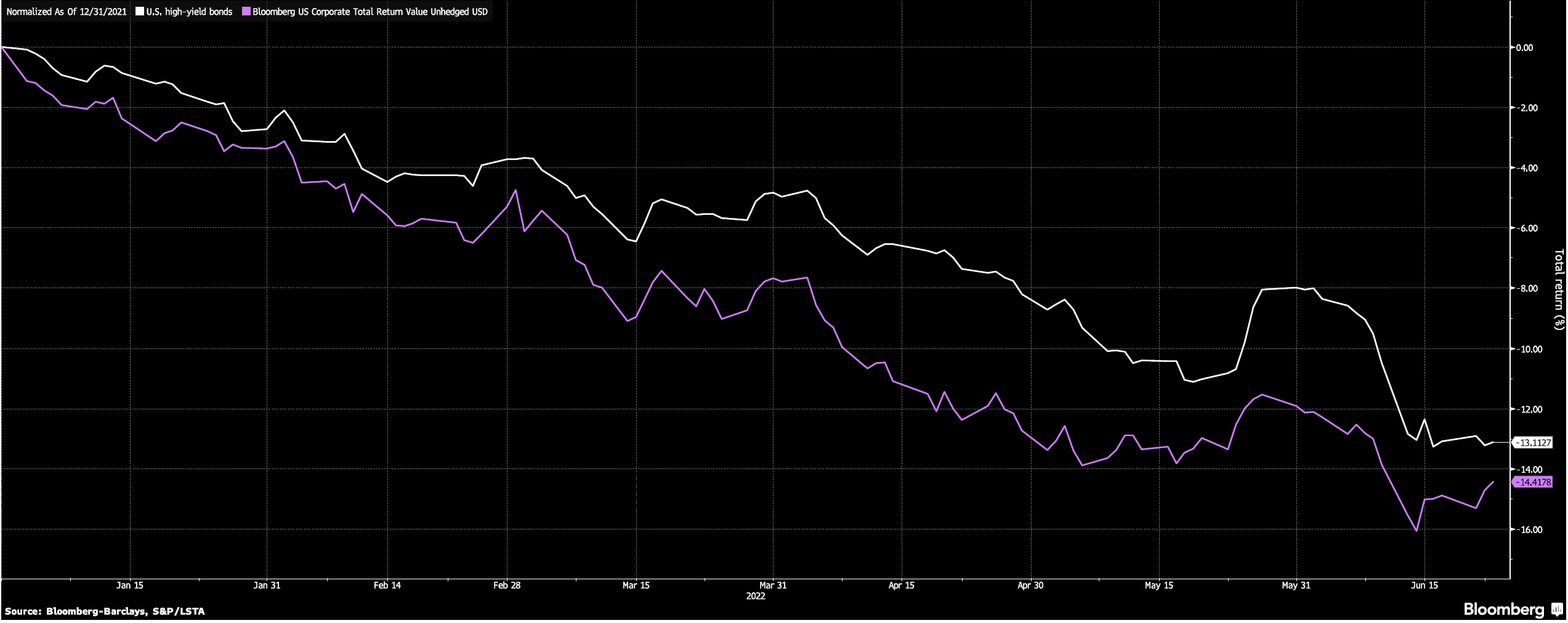

Lower credit ratings = higher risk = higher yields, hence the name given to high-yield bonds. But both high-yield (white) and investment-grade (purple) have fallen on a total return basis as shown below:

What we have seen now, is that investment banks are facing huge losses since prices of bonds are plummeting, and so when trying to offload corporate debt they are struggling, causing them losses. Banks are liable to cover the difference in price when they decide to discount the bond if already committed, minimising underwriting fees.

Recently, a deal for US firm 'Entegris' revealed a discount of 91 cents on the dollar for a bond underwritten at the end of 2021. The notional value of the bond was $895m, with a high coupon rate of 5.95%. The discounted price drove yields higher, and contributed to loses for underwriters amounting to over $35m. This goes to show the extent of the damage.

An almost bizarre situation can be seen with Alphabet, whose bonds with maturity in 2050 are trading at 65 cents to the dollar, an unprecedented 35 cent discount, from its issuance in August 2020. While this is an investment-grade bond, it is trading at such a low price, comparable to low-rated companies with much higher risks. The yields are significantly lower, at 4%, whereas many of the high-yield companies trade at over 15% yields.

It would be natural to think for the same price and higher yield, the lower-rated bond is an obvious choice. Even so, the investment-grade bond may be more attractive, given that with high-yield bonds, the risk of default is pertinent meaning yields are almost irrelevant. Therefore, a high-quality bond trading at the same price offers a greater rate of receiving the yield, being a more tempting option.

Corporate bonds are a steal right now; some companies may even wish to buy back their own debt whilst it remains cheap. However, until interest rates are lowered again, this discounting may remain, and this will inevitably happen, meaning the best time to take advantage of it is now.