Lira - Outlier Amongst the Rest

Volatility of the Turkish Lira

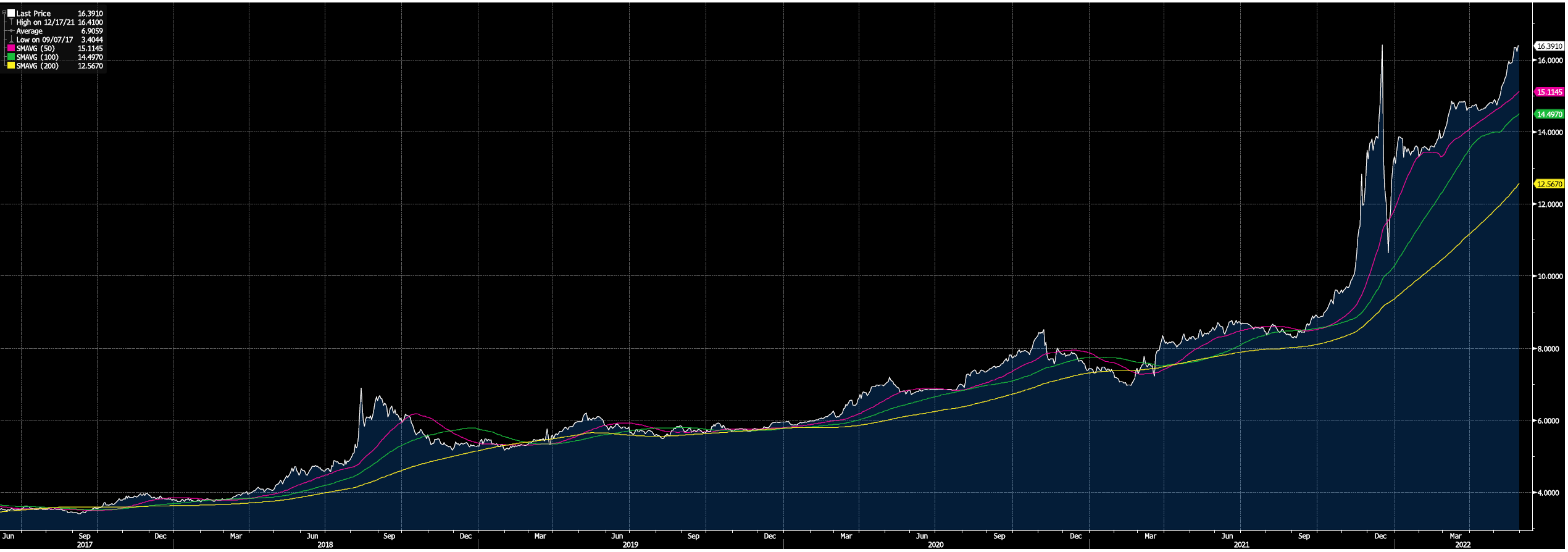

The Turkish Lira has had a volatile path since the inauguration of President Erdoğan in August 2014, the source of increased authoritarianism and unorthodox monetary policy in Turkey. The hits to the Lira have been extreme, with volatility in the currency being surpassed only by inflation fluctuations.

The 5-year spot price of the Lira has risen from 3.79TRY at the start of 2018 to 16.40TRY, as of 31st May 2022, displaying rapid depreciation, driven by a combination of several factors:

Monetary Policy

Turkey can be seen as an outlier in terms of its monetary policy compared to almost 50 other Central Banks’ responses. The Turkish Central Bank (TCMB) under Erdoğan has been notoriously hesitant to increase interest rates, stemming from the President’s underlying beliefs. The basis of these beliefs contradicts common Macroeconomic theory, as they enforce that higher interest rates will in fact increase inflation.

The foundation of these views is derived from 2 assumptions:

many Turkish businesses have high borrowing costs as a proportion of total costs

firms have enough pricing power to transfer higher costs onto consumers

Both in conjunction mean higher interest rates may cause runaway inflation, however this is already being aggravated due to the low and maintained interest rates. Inflation is currently at 69.97%, surging to these extreme levels, partly due to the unnatural monetary policy.

In an economic climate where over 50 Central Banks have increased interest rates, it seems bizarre Turkey has maintained its level at 14% for 5 months in a running, and it does not look likely to change. The FED in comparison have announced interest rate hikes, and those along with the BOE, are significant at that. It is true that interest rate changes will not have a homogenous impact everywhere, however the spiral in rising inflation does seem to be correlated with unchanged monetary policy, and so could point to a change needed.

Commodity Price Hikes

Turkey is a net importer of energy and commodities such as gold and iron. With commodity and energy prices through the roof, the Lira has suffered due to the budget deficit which has exacerbated in Turkey. This has led to a fall in demand for the Lira, due to fears of repaying. Falling demand for currencies depreciates the currency and has contributed to the crash of the Lira.

In March 2022, Turkey posted a deficit of 69 billion Liras, equivalent to $4.7 billion. This is a combination of consumer and government spending, both resulting in a deeper fiscal situation. This however, is a more recent phenomenon which has worsened the currency, rather than being the primary source of the decline in the Lira. Turkey ran a surplus in August 2021, November 2021, January 2022 and February 2022. And in the last 5 years, it has been in and out of surplus and deficit, meaning the Lira crisis which took-off around 2018 is unlikely to have been caused by the changing deficits, but may have been temporarily worsened recently.

Low International Reserves

Turkey has recently depleted a large proportion of its foreign currency reserves in attempts to stabilise the Lira, as Turkish businesses face the prospects of a depreciating currency, hoping to buy more dollars, to shield themselves from surging inflation.

In the 7 days till 13th May 2022, Turkish foreign currency reserves fell by $4.8 billion, decreasing the total to $62.2 billion. This is just part of a series of attempts to prop-up the Lira, with notable events being:

spent $7 billion in December 2021

spent $165 billion in the period 2019-2020

Both had little implications, as the Lira remains an unstable currency, however now there is an additional concern of not having enough reserves to act as a backstop for the Lira. The currency is now in a vulnerable and exposed position, with further pressure from inflation rates and commodity costs not helping.

Is the Lira doomed?

It seems without a monetary policy tool to stabilise inflation and hence the currency, as commanded by Erdoğan’s refusal to hike rates. This does not mean there cannot be recovery of the Lira. This has been proven in the past. Last year, Turkey introduced the FX-protected accounts, which have attracted an estimated 849 billion Lira ($53 billion), as of May 2022. This is a scheme to reverse dollarisation and support the Lira. It works by compensating individuals, if the depreciation in the exchange rate on current holdings exceeds the interest rate, with the cost being covered by authorities. While this scheme will allow for higher Lira liquidity, its compliance may be questionable, as depositors may not switch to these accounts if inflation rates remain high and increasing, scraping away at their real returns.

Having said this, installing confidence in consumers is key, and schemes such as this to support the Lira are vital, especially given the economic climate Turkey faces, with its monetary and fiscal policies.