Micro WTI Crude Oil Futures

Trade Idea

As we saw in 'Oil Market Update', there has been a significant rise in volatility of oil prices owing to a mix of supply and demand factors as well as investor sentiment.

With rising volatility we can make use of WTI Crude Oil products in order to enter a position which we may think benefits from the volatility. We focus on the WTI Crude Oil Future products but more specifically, the Micro Futures.

What Are Micro WTI Futures?

As an overview, a future contract is an obligation to buy or sell an underlying asset at an agreed price at a pre-specified date. The fix the price in the contract, and the buy or sell order is executed at expiry of the contract.

Now, a standard future contract on WTI Crude Oil is an obligation to buy or sell WTI Crude Oil at a pre-specified price at expiry of the future. Commodity markets in general utilise future contracts heavily as investors like to lock-in prices now, for future delivery. This is both to take a view and to hedge an underlying position.

Micro contracts are smaller-sized copies of their regular contracts. The Micro WTI Crude Oil Future is 1/10th the size of the regular future, trading in 100-barrel increments. What this means is it is more efficient and cost-effective for investors to access the oil market, which should increase liquidity and allow for more trading. The micro contract allows for weekly and monthly expiry, so there is greater flexibility and precision.

Most importantly, the micro contracts require smaller margin requirements which is beneficial for investors.

Micro WTI Crude Oil Future Options

Now we have our future contracts outlined, we move on to the product we will use to position ourselves in the face of volatility in the oil market.

As we have discussed, option contracts are a type of derivative which are extremely diverse and allow for a low-risk option, due to the removal of the obligation to execute a buy/sell order at expiry.

We will use options which use the Micro WTI Crude Oil Futures as their underlying contract. Like their standard option contract these are also 1/10th of the size.

Premium

The premium of the Micro option differs slightly from the standard contract due to the multiplier differential.

The premiums are quoted in 1 cent per barrel tick increments. This means 1 tick move = $1 move.

To see this in an example:

Premium of the Micro option = $0.70

Cost of option = $0.70 * 1 * 100 barrels = $70

What Strategy Can We Implement?

Now we have our product to be used outlined. Now we just need a strategy.

As we suggested in the oil market update, it is tricky to conclude a directional move for the WTI Crude price. The major forces at play over the next few weeks will be:

Slowing demand from new variant outbreak in China and concerns over implications for the opening of the Chinese economy. The recent outbreak facing China has been crippling and while China has suggested its Zero-Covid Policy will come to an end, the extent to which this is possible is not hopeful. Concerns over global outbreak will be in the forefront of people's mind, which may prevent the re-opening of the economy at a desired pace. Being a heavy importer of oil, there may continue to be diminishing demand of oil, which contributes to falling prices.

US buyback of oil to replenish its Strategic Petroleum Reserve. With price of oil falling significantly YTD, and the US contributing heavily to this by depleting its Reserve below 400m barrels. If the US is looking to add to the Reserve, this means there will be less supply of oil in the market coming from this source, and so higher prices. The US suggests this will encourage domestic production, however the extent to which producers are confident enough of demand is yet to be seen.

Rising uncertainty as we approach the peak of Winter. We are just one month into Winter and the worst may be yet to come. The rising uncertainty was seen with average CVOL levels over twice as higher than pre-Covid levels. However, we may see this rising further if there is increasing uncertainty over supply coming into the winter months. Low demand driven by these concerns of economic instability contributes to plummeting prices.

As we can see, there is no clear conclusion of whether we expect prices to increase or decrease. Therefore, the best strategy will use this idea.

Something which we can talk about, however, is volatility. While we may not be able to predict the price movement, we may be able to predict the volatility movement. All the above factors are likely to contribute to higher volatility. There is still a lot of uncertainty over demand and supply and without confidence there will likely be rises in volatility.

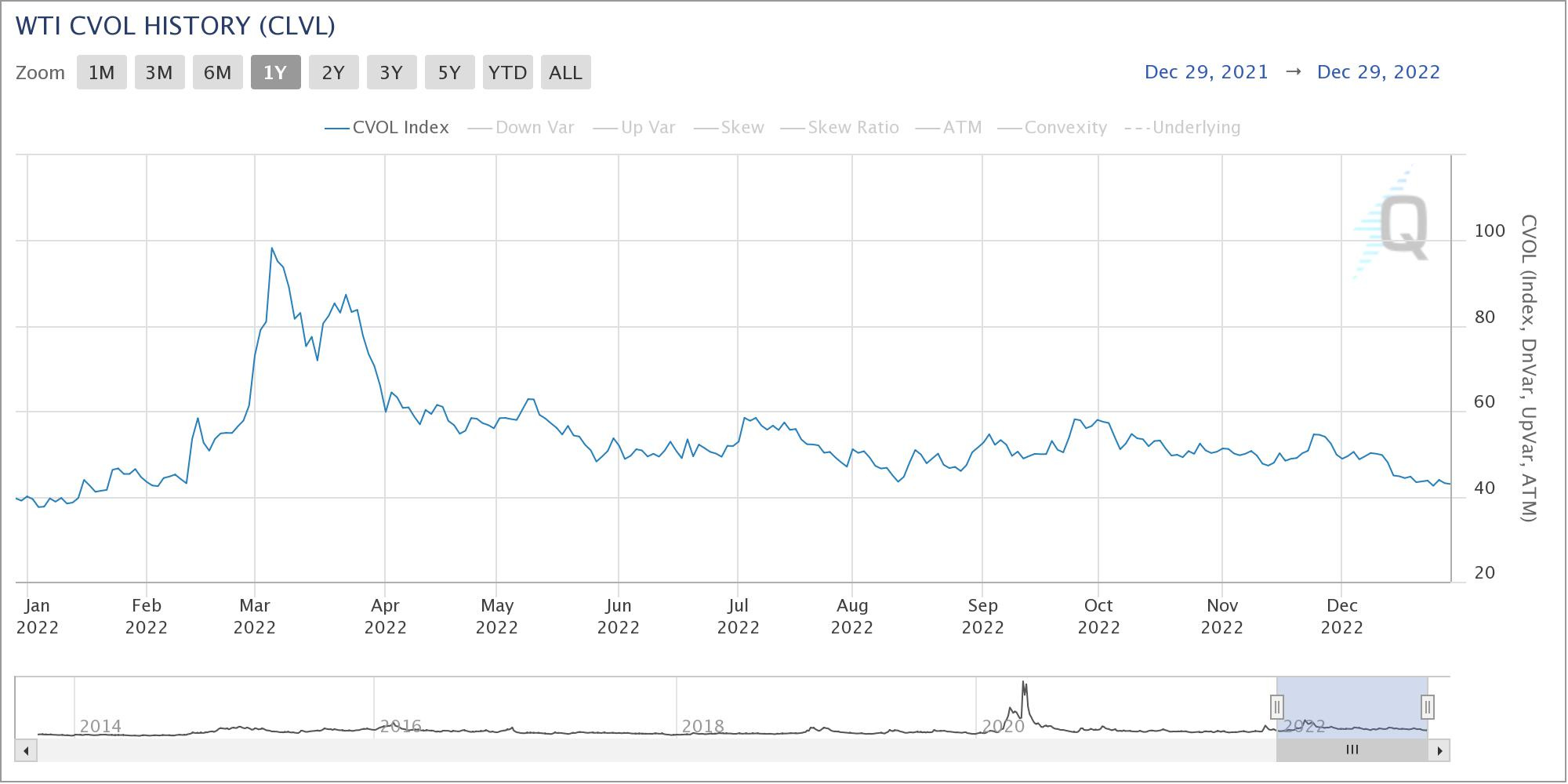

A 1-year graph of the CME's CVOL for WTI Crude can show the pattern of volatility this year. If we zoom in to December 2022, we can see it is below the trend line for 2022 in general for April - November. We may believe this is an inaccurate depiction of the current market climate, and given the above events actually expect the CVOL index to rise.

So our strategy is based on rising volatility, and a price movement which we are unsure of (up or down). Therefore, we can work with the Micro WTI Crude options to devise a trade.

Trade Idea

What we can implement is a strangle position. This is a combination of option contracts such that we buy a call option at a high strike price and buy a put option at a low strike price. The commonality between these two is the expiry date and the underlying asset.

The position benefits if there are large price movements in either direction from the strike price, and so it is a bet on volatility rising and a price movement in either direction, exactly the position we want to hold.

In addition, we can see the CVOL looks low at the moment, and so this idea supports an increasing CVOL index.

An ATM (at-the-money) option on the WTI Crude Oil Future currently has a strike price of $80.

We therefore choose a strangle position that is situated either side of this strike, so we need a lower strike for the put and a higher strike for the call.

The contracts we want to buy are:

$74 OTM Put Option with a premium of $0.77

$86 OTM Call Option with a premium of $0.61

Both have an expiry of February 2023 (monthly European option) and are on the WTI Crude Oil Future underlying. We want to buy OTM options so that the price moves towards one side and the profits of that leg outweigh the losses from the other leg.

Net Premium:

$0.77 * 1 * 100 = $77

$0.61 * 1* 100 = $61

Net premium paid = $138

How Will I Be Profitable?

There are different cases in which the position will be profitable:

CASE 1: WTI Crude Oil = $90

: Time to expiration = 2 weeks

The price of WTI Crude has risen, past the 6 point interval of the strangle position either side of the ATM strike

The call option is now ITM

An ITM option's premium will be higher than the premium of any other option, as there is a much greater chance of making a profit at expiration

The put option is further OTM and the premium will fall

Sell the ITM call option for a premium of $4.80 (estimation based on current ITM call option premiums)

Sell the OTM put option for a premium of $0.13 (estimation based on current OTM put option premiums)

Alternative was to hold the strangle position to expiry, in which case the call option would yield ($90-$86) = $4. The put option would expire OTM and will be worthless

Net Premium Received = ($4.80 * 1 * 100) + ($0.13 * 1 * 100) = $480 + $13 = $493

NET PROFIT = $493 - $138 = $355

CASE 2: WTI Crude Oil = $70

: Time to expiration = 2 weeks

The price of WTI Crude has fallen, past the 6 point interval of the strangle position either side of the ATM strike

The call option is now even more OTM

The put option is ITM and the premium will rise

Sell the OTM call option for a premium of $0.06 (estimation based on current OTM call option premiums)

Sell the ITM put option for a premium of $6.43 (estimation based on current ITM put option premiums)

Alternative was to hold the strangle position to expiry, in which case the put option would yield ($74-$70) = $4. The put option would expire OTM and will be worthless

Net Premium Received = ($0.06 * 1 * 100) + ($6.43 * 1 * 100) = $6 + $643 = $649

NET PROFIT = $649 - $138 = $511

The extent of profits depends on the volatility of the price movement. If the price does not move enough, then the premium paid for the position will be higher than the return and the position will result in a break-even position or a loss:

CASE 3: WTI Crude Oil = $83

: Time to expiration = 2 weeks

The price of WTI Crude has risen, but not past the 6 point interval of the strangle position either side of the ATM strike

The call option is still OTM

The put option is further OTM and the premium will fall

Sell the OTM call option for a premium of $1.08 (estimation based on current ITM call option premiums)

Sell the OTM put option for a premium of $0.30 (estimation based on current OTM put option premiums)

Net Premium Received = ($1.08 * 1 * 100) + ($0.30 * 1 * 100) = $108 + $30 = $138

NET PROFIT = $138 - $138 = $0

We can see that the smaller the price movement of the WTI Crude, the less profit the strangle position makes.

However, given the market conditions, we expect there to be a rise in CVOL which will be accompanied by a fluctuation in prices either higher or lower than current. We believe the strangle position is a good entry to gain exposure to the oil market volatility.