Sri Lanka

A Family Tree Cut at its Roots

Political turmoil. Economic distress. Fuel shortages. While many countries now fit these descriptions, there is one that has arguably seen the largest failure to manage these. Sri Lanka has historically been a country led by the Rajapaksa family for much of the last 20 years, and while the family is flourishing and eating off the spoils, it is indeed every citizen that has been burdened by this. Questions have been raised as to whether nepotism has played a role in President Gotabaya Rajapaksa's term, claims of which unsurprisingly have been denied.

Sri Lanka drained its government revenue and took on immense amounts of debt (pre-pandemic), which only worsened the economic climate once the pandemic collapsed foreign currency earnings, and global inflation hit consumers hard.

Paying back sovereign-debt instead of defaulting and using the minimal reserves to pay for basic imported necessities was a mistake, which has led to Sri Lanka not able to pay for any fuel imports, as there are no usable foreign reserves to do so. For an island, especially, this is detrimental, and the people of Sri Lanka are suffering the most.

Protests on the residents of President Rajapaksa and Prime Minister Wickremesinghe have highlighted this clearly.

Economic Climate

Inflation in Sri Lanka for June 2022 reached an astonishing 54.6% YoY, which led to a 100 bps increase in the interest rate as well, standing at 15.5% as of 7 July 2022.

While this will draw more funds to the banking sector, it adds to the already long list of economic difficulties.

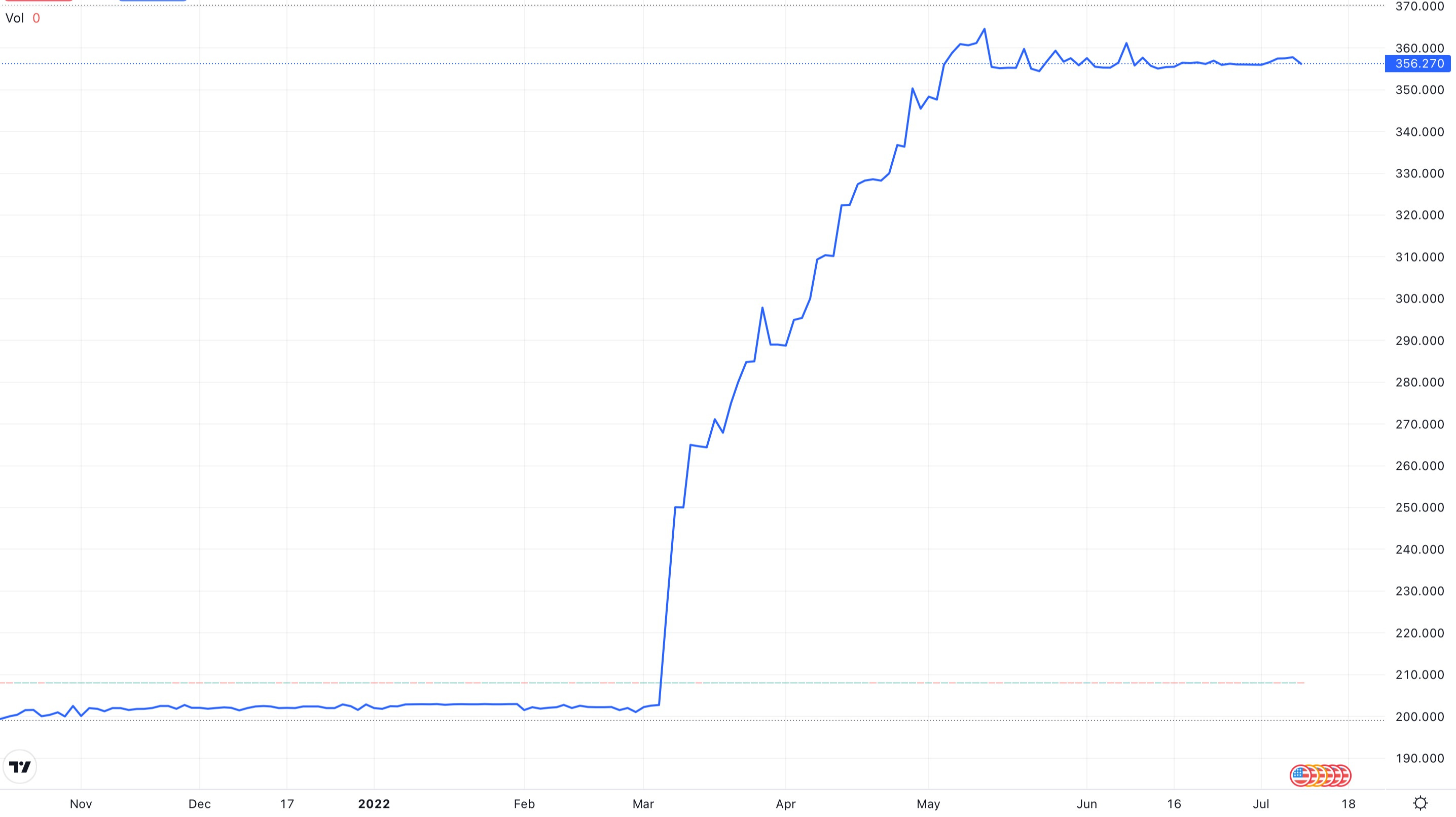

This can be seen well through the USD/LKR plot. Investors priced in severe depreciation of the Sri Lankan Rupee (LKR) since the suspension of debt payments, which up till now has led to the rise in the currency pair (YTD).

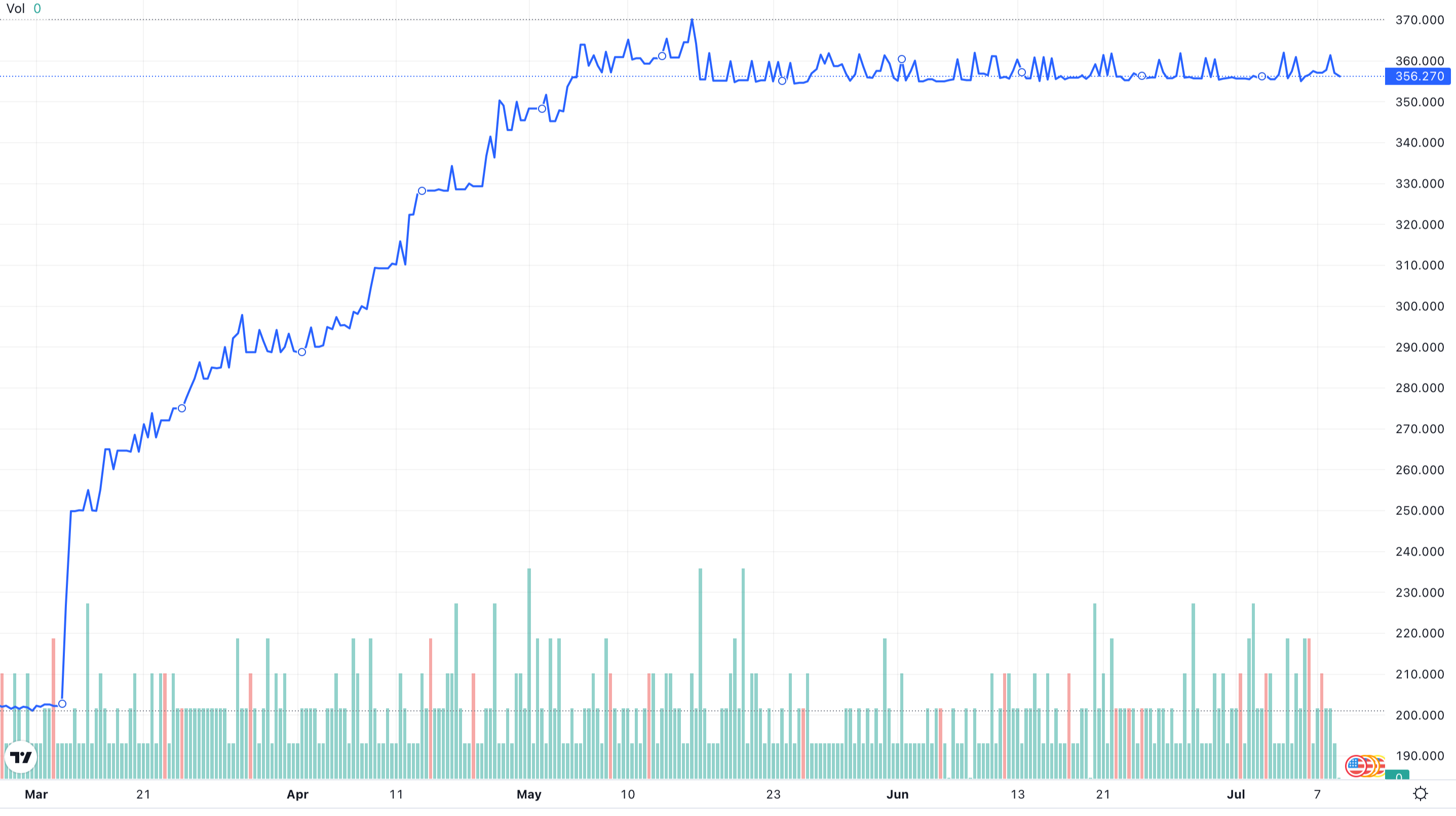

However, what is even more interesting to note is when we zoom in more:

This shows us the volatility in the currency pair between mid-May and present; reflective of the country's political climate in fact. With a default priced in, there is no more movement for further currency depreciation for the LKR.

Debt Obligations

In April 2022, Sri Lanka decided to suspend foreign debt repayments. In May 2022, Sri Lanka defaulted.

Bailout packages from the IMF are in discussion. With about $45bn of long-term debt outstanding ($8bn maturing in 2022), considerable and indeed believable reforms are needed to ensure the IMF the funding will be used meaningfully. Whether this takes the form of higher public taxes, lower public spending is unknown.

However, it seems unlikely higher public taxes will cool down any tension in Sri Lanka at the moment. People are angry, lacking basic necessities and have no belief in the government. Both the PM and President have agreed to quit, and the political turmoil that will inevitably follow is not helping.

Debt-for-Nature Swaps

An interesting proposal by the Government is to engage in debt-for-nature swaps. These essentially mean some loans and outstanding debt is forgiven if instead there is investment into sustainable projects and environmental conservation.

For a country rich in wildlife and forestry, this does seem like a promising request, and might some load off their shoulders.

Restructuring debt is an unsustainable measure to provide short-term relief, and so it is necessary to utilise methods of reducing the total burden; not just shift it to the next generation.

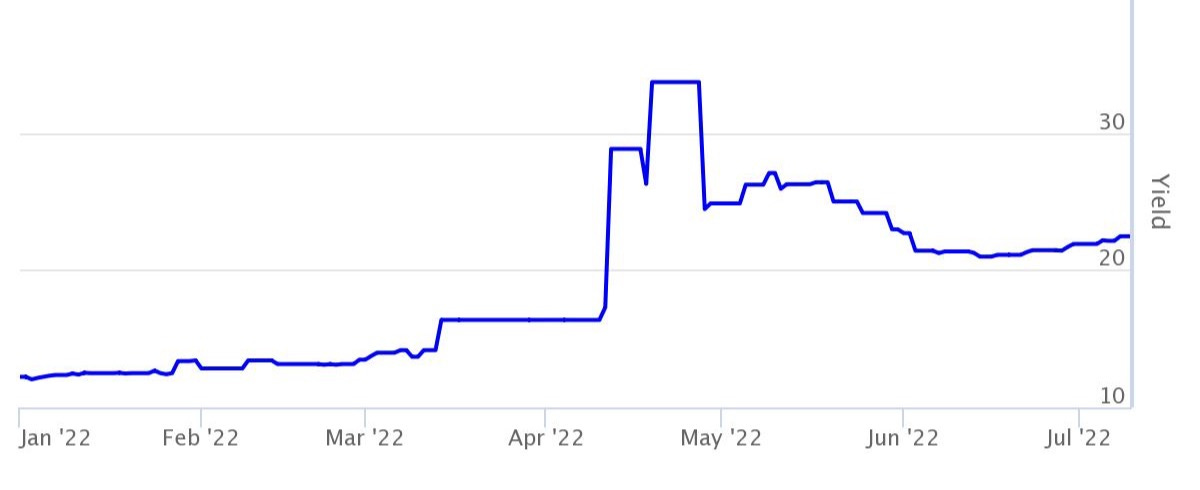

Yields

The 10-year Government bond yield helps us visualise the picture well:

Current yields stand at 22.08%, one of the highest in the world, as of 10 July 2022. Higher yields are indicative of riskier government bonds and higher chances of default - in-line with what we have seen so far. The peak was between April and May 2022, when speculation of a default drove these yields up and up.

Currently, the outlook seems to point towards higher yields from 22.08%. It is hard to predict how political turmoil, global supply chain issues, fuel shortages, inflation and foreign-reserve depletion (to name a few) will all fit together. The time it will take for the IMF to bailout Sri Lanka, for them to decide a new cabinet and to start the recovery of the Government, yields are likely to increase. It is likely the yields will increase towards the low 30s%, the levels seen during the risk of default, however it is unlikely to break-through this level if the road to recovery is initiated.