Volatility: Predictive Power?

VIX Index Trade Idea

Volatility in the markets is understood as the rate at which the price of a stock or an asset increases or decreases over a certain period of time. An extremely versatile measure, it helps to gauge market sentiment by seeing how fast prices are changing.

Derived from this is the Cboe Volatility Index (VIX).

The VIX is an index measuring market's expectations for relative strength of near-term price changes of the S&P500 (SPX)

Encompassed in the price of equity options, through the Black Scholes model, is the volatility of a stock price move. Therefore, since the index is derived from the price of options expiring in the near-term, it calculates a forward volatility estimation. The standard period of time is a 30-day forward value.

The VIX can be used in two main ways:

Investors can take a position on volatility and use VIX-linked instruments to gain volatility exposure

Investors can use the index as a predictive power tool over economic situations

Examples of such instruments include futures and options on the index.

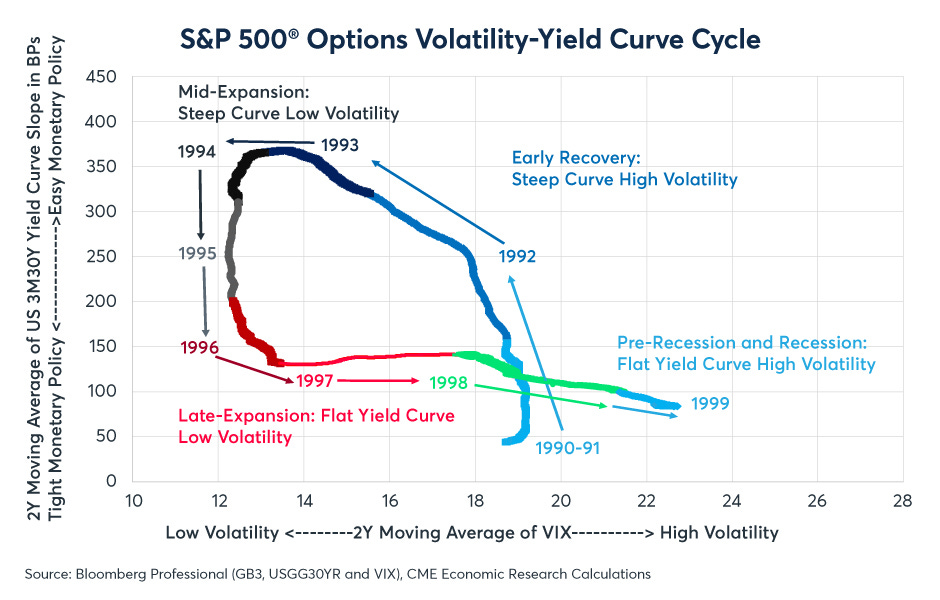

But what has been an interesting trend is the correlation that the VIX has with the yield curve.

VIX and Yield Curve

The correlation between these two indicators has been tracked closely, and a powerful pattern has been noted. A cyclical pattern has risen, which is predictive of recessions - powerful indeed.

The trend is as follows:

Economy starts with steep yield curves and high volatility in the recovery period after a recession. Persistent fears over market sentiment due to back-end of recessions keep volatility high. Short-term yields are lower than long-term yields due to monetary policy easing, so we see steep yield curves (typically 3m30y), as Central Banks start to stimulate the economy

Injections through quantitate easing means lowers volatility (and the VIX) as greater confidence by investors. Generally stable market conditions keep volatility low and yield curves steep

Central Banks start to tighten monetary policy, however does not immediately transmit into a recession as there are lags in the economic cycle. Volatility does not pick up as the effects of the monetary policy change are not significant in terms of credit concerns. Higher rates leads to flatter yield curves.

Higher rates reverberate into greater recessionary risks and economic downside, lifting volatility levels. Yield curves remain flat and the economy enters a recession. The cycle repeats after this from stage 1.

We see the VIX and yield curve relation is therefore historically predictive of recessions - however what we have seen in the last 2 years is very contrary to this traditional view. High inflation and low rates have prevailed recently, but now the yield curves have and we believe will continue to flatten. See ‘Trade Idea: 10s30s Steepener’ for further context on this. In addition, heavy fiscal expansion has been an unprecedented addition. All this in the face of high volatility makes the cycle seem to have broken-down, as Central Banks also rely solely on data-driven metrics as the best judge of near-term policy rate changes. This has exacerbated volatility, and so the historical trend we see may not hold as strongly anymore.

Does this still hold?

Mary Daly of the San Francisco FED came out this week stating the market severely undervalues the FED's strong commitments to continue to hike rates. She said the market's pricing of rate cuts is a disconnect from reality, with the urgency for the FED to control and subdue inflation the top of its mandate.

And this week, the German Central Bank states that there is continued inflationary pressures facing Germany and Europe in general, due to squeezes in Russian gas supplies. The suggestion we are not near the peak of inflation suggests interests will continue to rise.

However, this provides a conflict of interest, since rates need to fall in a recessionary environment in order to ensure we do not enter a situation of unrecoverable economic downturn and loss-spirals. With rates needing to be cut, but unlikely they can be, we are likely to see volatility and the VIX rising further.

It is hard to say where yields will move in the next FED or ECB meeting, let alone a 1y forward calculation. But we can bet on volatility increasing as a result.

Trade Ideas

We may consider a trade to take advantage of rising volatility. We can buy VIX futures, or we can buy VIX call options. Call options may be a safer option, given the downside protection options inherently offer.

Either choice however positions us to long volatility, with exposure to pure vol.

To further the trade, we may consider purchasing a put option on the VIX if we see volatility falling. When volatility is low, put option premiums will be lower, and so we can strategically buy at a lower premium. Current VIX is just under 21, at 20.60, which we believe is low and will rise. Put premiums should be relatively cheap now, and so we can purchase put options to hedge the downside risk as well.

A strangle position (assuming we purchase the put and call at different strike prices) therefore sets us up to profit from rising volatility, which we believe is consistent with current market conditions.